Contribution margin income statement, the output of the variable costing is useful in making cost-volume-profit decisions. It is an important input in calculation of breakeven point, i.e. the sales level (in units and/or dollars) at which a company makes zero profit. Breakeven point (in units) equals total fixed costs divided by contribution margin per unit and breakeven point (in dollars) equals total fixed costs divided by contribution margin ratio. As you will learn in future chapters, in order for businesses to remain profitable, it is important for managers to understand how to measure and manage fixed and variable costs for decision-making.

Fixed Cost vs. Variable Cost

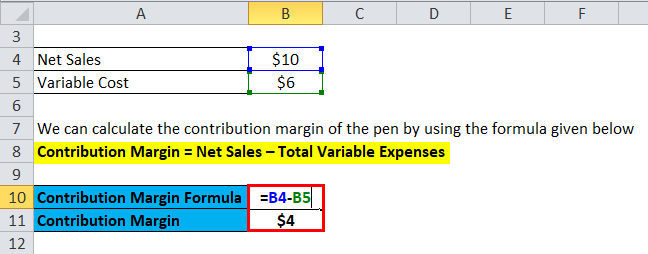

The Contribution Margin Ratio is a measure of profitability that indicates how much each sales dollar contributes to covering fixed costs and producing profits. It is calculated by dividing the contribution margin per unit by the selling price per unit. As mentioned above, the contribution margin is nothing but the sales revenue minus total variable costs. Thus, the following structure of the contribution margin income statement will help you to understand the contribution margin formula. The contribution margin is important because it helps your business determine whether selling prices at least cover variable costs that change depending on the activity level.

How to calculate contribution margin

This demonstrates that, for every Cardinal model they sell, they will have \(\$60\) to contribute toward covering fixed costs and, if there is any left, toward profit. Jump, Inc. is a sports footwear startup which currently sells just one shoe brand, A. The sales price is $80, variable costs per unit is $50 and fixed costs are $2,400,000 per annum (25% of the which are manufacturing overhead costs) . If total fixed cost is $466,000, the selling price per unit is $8.00, and the variable cost per unit is $4.95, then the contribution margin per unit is $3.05. The break-even point in units is calculated as $466,000 divided by $3.05, which equals a breakeven point in units of 152,787 units.

Company

In the past year, he sold $200,000 worth of textbook sets that had a total variable cost of $80,000. Thus, Dobson Books Company suffered a loss of $30,000 during the previous year. Contribution margin is used to plan the overall cost and selling price for your products. Further, it also helps in determining profit generated through selling your products. The contribution margin is affected by the variable costs of producing a product and the product’s selling price. For example, if sales double, variable costs double too, and vice versa.

- Fixed costs are the costs that do not change with the change in the level of output.

- We may earn a commission when you click on a link or make a purchase through the links on our site.

- Now, the fixed cost of manufacturing packets of bread is $10,000.

- Cost accountants, financial analysts, and the company’s management team should use the contribution margin formula.

- Calculating the contribution margin for each product is one solution to business and accounting problems arising from not doing enough financial analysis.

However, ink pen production will be impossible without the manufacturing machine which comes at a fixed cost of $10,000. This cost of the machine represents a fixed cost (and not a variable cost) as its charges do not increase based on the units produced. Such fixed costs are not considered in the contribution margin calculations. Similarly, we can then calculate the variable cost per unit by dividing the total variable costs by the number of products sold. The contribution margin is the leftover revenue after variable costs have been covered and it is used to contribute to fixed costs.

Do you already work with a financial advisor?

If they sold 250 shirts, again assuming an individual variable cost per shirt of $10, then the total variable costs would $2,500 (250 × $10). Here, the variable costs per unit refer to all those costs incurred by the company while producing the product. These include variable manufacturing, selling, and general and administrative costs as well—for example, raw materials, labor & electricity bills. Variable costs are those costs that change as and when there is a change in the sale. An increase of 10 % in sales results in an increase of 10% in variable costs.

For League Recreation’s Product A, a premium baseball, the selling price per unit is $8.00. Profits will equal the number of units sold in excess of 3,000 units multiplied by the unit contribution margin. Now that we understand the basics, formula, and how to calculate per unit contribution margin, let us also understand the practicality of the concept through the examples below. Let us understand the step-by-step process of how to calculate using a unit contribution margin calculator through the points below. Let us understand the formula that shall act as a basis of our understanding of the concept of per unit contribution margin through the discussion below.

Direct variable costs include direct material cost and direct labor cost. Cost accountants, financial analysts, and the company’s management team should use the contribution margin formula. CM is used to measure product profitability, set selling prices, decide whether to introduce a new product, discontinue selling a specific product, or accept potential customer orders with non-standard pricing. what is trade discount journal entry examples calculator The CVP relationships of many organizations have become more complex recently because many labor-intensive jobs have been replaced by or supplemented with technology, changing both fixed and variable costs. For those organizations that are still labor-intensive, the labor costs tend to be variable costs, since at higher levels of activity there will be a demand for more labor usage.